|

Phone: 888-262-7171 Email: support@thesmartermerchant.com Learn More |

Since: March 2021 Since: March 2021 |

Stories

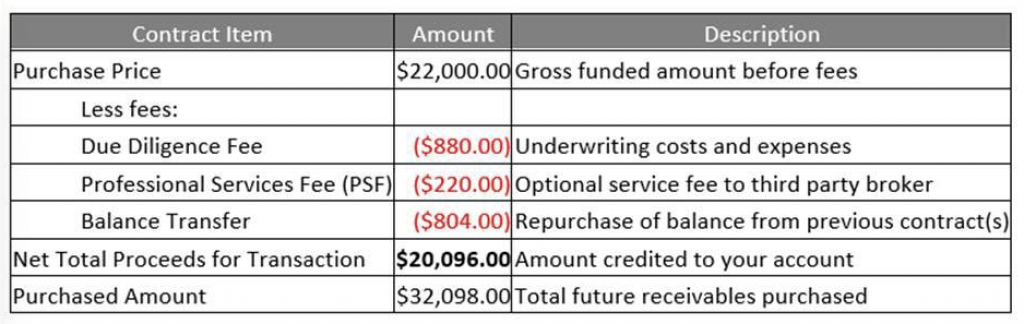

Yellowstone Capital Introduces a Smarter Box In Move Towards Transparency

September 26, 2018Yellowstone Capital CEO Isaac Stern announced a “Smarter Box” through social media channels this morning. The itemized box will be provided to merchants through a post-funding email as part of a company effort to maximize transparency.

According to the announcement:

“[We are] very serious about maximum transparency and disclosure to our funding partners’ great merchant customers. In addition to our new Purchase and Sale Agreement we will be using with each of the funding partners on our platform, we are also implementing a transaction summary email to ensure that all applicable fees, costs, disbursements and hold-backs are clearly understood by all parties. Our new contract will increase disclosure while simplifying the product, while our summary confirmation ensures greater understanding and improved communication between our funding partners and their customers.”

Example of the box:

Based in Jersey City, NJ, Yellowstone Capital has originated more than $2 billion to small businesses since inception.

Merchant Cash Advance Accounting Q&A

May 25, 2016

As a successful and knowledgeable Merchant Cash Advance accountant I often receive questions from MCA business owners and syndicators. In the last tax season, my accounting firm recognized that many of the questions we receive are distinctly similar. In the following article I address the most common questions my accounting office receives.

Question #1: When I am accounting for my Merchant Cash Advance company isn’t a cash advance accounted for in the same way as a loan? It looks the same on a spreadsheet so isn’t the interest calculated in the same way as a normal loan?

Yoel Wagschal CPA: No. Merchant Cash Advance companies do not have interest. If you have interest then what you have is a loan business, not a Merchant Cash Advance business. Loans use an entirely different method of accounting. If you are still accounting for your Merchant Cash Advances as loans with interest then you will have regulatory issues. If you tell an IRS agent that you are not a loan company but they see your books are exactly like a loan company, how do you think that will end for you? Loans and interest are in a different world. You are the last person who wants to combine those two worlds. You need to see how they do their books at an accounts receivable factoring company and model yourself after them. They do it the way my accounting firm presents it.

Question #2: Your article mentions two ways in which Merchant Cash Advance Companies can account for transactions (cash basis and accrual). Are those the only two ways in which my accounting can be processed?

Yoel Wagschal CPA: I guarantee you would have a big argument if you brought 100 accountants together and asked them all this question: How do I recognize revenue in an accrual basis (from a GAAP standpoint) if I am allowed to take the entire income this year? You would have all kinds of voices and differences of opinions because there is no guidance for this industry. I have done the research and structured an accounting methodology. I’ve spoken with the biggest firms and dealt with the biggest names in this industry. I do have a passion for MCAs. When it comes to a tax standpoint, if you file a cash basis and you want to minimize your exposure, there is really only one way to do it. Those two ways (cash and accrual) can be kept so that they are converted from one to the other at the end of the year. Hence, if you want to prorate the income portion of your receivable (cash basis) I would still keep the books on accrual then convert it at the end of the year. You could do this with a single journal entry because it simplifies the bookkeeping process. You end up with an accrual basis financial statement and a cash basis tax return.

Question #3: I keep being told that my tax liability is based on the difference between what I spend (including funding merchants) and what I receive. For example, if we fund 100K and collect 140K in 140 days how should we keep our books? Right now we don’t recognize any income until we get back the initial funding, even if we renew the merchant over and over. Please elaborate on how revenue should be accounted for. I want to minimize my tax liability but I also want to be sure that this is the correct way to go about it.

Yoel Wagschal CPA: I have a very simple quiz:

YWCPA: Do you trust your accountant?

MCA: Yes. Yes, I do.

YWCPA: You should not. Even if you were my own client I would tell you the same thing. Why do you trust your accountant?

MCA: Because they are a professional. This is what they went to school for. This is what they do for a living.

YWCPA: Do you consider yourself a smart person?

MCA: Yes, I do.

YWCPA: Is it possible that you are smarter than your accountant? Is it possible that they simply learned a different trade than you?

MCA: Yes, that is possible.

YWCPA: Ok, then you should use your own IQ to see if what your accountant says makes sense. If your accountant tells you something that doesn’t make sense about your own business, and you believe your accountant because this is their job then you are not using your high IQ. This is especially true if you have strong negative feeling towards what you are being told. I am not telling you to jump to conclusions. I am saying you should ask questions. Think about this for as long as it takes. Your accounting should be clear and understandable to you.

I am a college professor. When I teach the principals of accounting I always start with debits and credits. I start here because students must know this concept through and through in order to be good accountants. It is the basis of all accounting. New students struggle with the logic behind this principle and I always respond that there are two options: The first option is simply to trust me. They can memorize the information and never know what it means. The second option is to completely understand. This is the option that both my students and Merchant Cash Advance business owners must choose. You, as the business owner, must understand where your own numbers come from. You must understand the foundation of your own accounting. You are entitled and responsible to understand it because of what you must sign on your company’s tax returns.

YWCPA: Do you know what you are signing on the tax return?

MCA: Do I know…?

YWCPA: Do you know what the fine print says directly above where you sign? It says:“Under penalty of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief they are true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.” That is what you sign. Now, do you know what the preparer has to sign?

MCA: The same thing…?

YWCPA: The preparer signs an acknowledgement that they got paid! What I am saying is that you, the business owner, is ultimately responsible for the numbers that are on your tax return. It is you, not the preparer, who certifies that the numbers are legitimate. Of course, accountants are bound by Circular 230 and code of ethics but the level of responsibility is much higher proportionately to the tax payer than to the tax preparer.

Recognizing income only when a deal pays off is clearly, in my humble opinion, “Fraud and Tax Evasion”. I would not sign off on such a tax return. It goes even further that a lot of people who are saying this type of stuff will add that a renewal is an extension of payment and you don’t have to recognize this until the renewal is completely paid off. In this theory you can be in business for 50 years making billions of dollars and pay zero tax. If you were an IRS agent, would you accept that position?

MCA: Mmmm… What’s your point?

YWCPA: Just answer the question. If you were the IRS agent, would it help if the taxpayer told you “my accountant said it was fine”?

MCA: NNNnno.

YWCPA: That’s my point.

Question #4: When my company advances funds to a merchant how do I account for this? Also, how do I account for my company’s income with cash basis (tax return)?

Yoel Wagschal CPA: Ok, we know that in cash basis accounting we don’t recognize revenue before it is actually received. For instance, a grocery store that lets a customer take an order on credit doesn’t recognize revenue at that point. Income is recognized when funds come in.

Now we will think about the Merchant Cash Advance industry. Let’s start with when you advance funds to a merchant. For this example you advance 100k to a merchant and the payback is 140k. The 100k you send to that merchant should not be expensed. That 100k should stay on your balance sheet. You don’t recognize any income because you haven’t collected any income yet.

At the end of the year we have collected half of the advance. It started with 100k funded and 140k to collect. Now we have collected 70k. The most rational way to decide which part of the 70k goes down on the balance sheet and which part should be recognized as income is to prorate it. You should show that half has been collected which means that half of your income should be recognized now. We show it now because you have, in fact, collected revenue.

Question #5: For cash basis (tax return) purposes, when do we realize a loss? How do you show and what do you call the write off of uncollectible merchant cash advances?

Yoel Wagschal CPA: This is a very good question. There are some weird things going on in this industry because normally in a business you don’t exchange money to make money. On a cash basis tax return you would not see a receivable on the cash basis balance sheet. Concurrently, you would not see any bad debt.

Bad debt is usually not something that you see on a cash basis tax return. However, if you really look at the IRS regulations they do understand that even in a cash basis business there are bad debt expenses. Why wouldn’t you usually see bad debt expense? It is because you never recognize any income from the money you didn’t receive. Even with a cash basis tax payment, when a taxpayer lends money to a vendor (in a ‘normal business situation’) and that vendor doesn’t pay the taxpayer back, we know the taxpayer is entitled to take a bad debt expense.

In the Merchant Cash Advance situation, where we exchange money to make money, what could be more of a ‘normal business situation’? This is how your business works so if a merchant does not pay you back then you are entitled to a bad debt expense (of course, the actual realizable cash loss). This bad debt expense gets realized when the Merchant Cash Advance company is certain they are not going to get paid. In the rare situations where you have already written off a bad deal and the merchant does end up paying, you will need to reduce your bad debt expense for the following year or you can add it to your income for the following year.

As far as labeling, I believe the IRS wouldn’t care what you call it. I understand why you want to label it differently. The truth is that this comes only out of the fear that an amateur might look at it. A real trained knowledgeable professional will understand it. Bottom line is, it is perfect (although not normal) for a cash basis taxpayer to have a bad debt expense. But, you can see nothing here is the norm. So do we care for the amateur or for the expert?

Question #6: (This is for “syndicators” which we define here as entities who provide funds to MCA companies before those funds are sent to merchants). Should I do my books whenever I get a payment, week to week, or in one lump sum? From a GAAP or accounting perspective do we use immediate revenue recognition or the deferred method?

Yoel Wagschal CPA: If you want to simplify your bookkeeping I suggest after the fact accounting. Just be sure to maintain absolute consistency. At the end of the year your accountant should be able to take your information, adjust it to a proper trial balance, and create your year end reports. However, if you do not maintain the highest degree of accuracy and consistency then your accounting work will be much more time consuming and potentially flawed.

In my office we have all different types of clients. We have clients who want their books maintained on a live basis. This means we are responsible for taking the information off their MCA platforms and processing it in the accounting system.

We also have clients who want weekly reports. This is a more tempered measurement of the MCA activity. It paints the MCA picture in broader strokes while still maintaining absolute control where tax liability is concerned.

Finally we have clients who only want monthly or yearly reports. This almost completely separates the deal-to-deal MCA activity from the accounting activity. It leaves my accounting firm with the responsibility of tax liability and accounting while the MCA company does their own MCA deal tracking. Whichever approach works best for the individual companies is what you should choose.

In all of these cases there is one fundamental accounting rule and that is 100% consistency. I teach all of my clients to be very disciplined. We recommend having one bank account that is strictly used for funding and receiving money and a completely separate account for operations. For the larger clients we recommend they fund from one account and receive in another account. There is no problem shifting money between these accounts because when an accountant looks at your books it is very easy to follow your transactions.

After you have separated the accounts we can do the actual accounting work for you. However, as we are about to explain the basic journal entries for MCA accounting we caution you to remember this ‘Breaking Bad’ example. In the TV Show Breaking Bad the show’s star (Walter White) explains why he is irreplaceable. Someone else cannot simply step in and recreate his product. His argument is that he is a chemist with multiple advanced degrees as well as years of experience and research. He cannot simply impart all of the knowledge he has to someone in a matter of days. No one can match his intellect simply by watching his actions. His explanation is that a less experienced person would not be able to know if something was off. How would a less experienced person know if one of the ingredients was the wrong type? How would they know if the temperature was slightly off or the cooling phase took too long?

The same practical concept must be applied here, when you are doing the accounting for your MCA transactions. If there was an error in the journal entries, if a procedure was misunderstood and then applied over and over again, if a large transaction was classified incorrectly – how would you know? Only a highly skilled accountant with knowledge of the MCA industry will be able to look over your work and make sure that all of the procedures have been followed correctly. We are about to provide the most basic journal entries for MCA accounting. However we insist you use caution in implementing these entries. We stress that you should consult with a trained accountant who can understand the procedures and recognize mistakes.

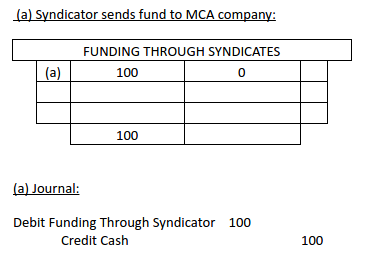

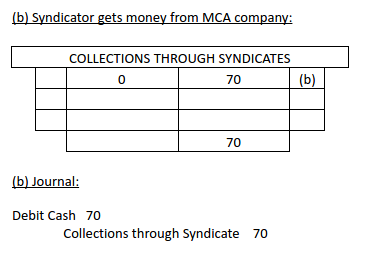

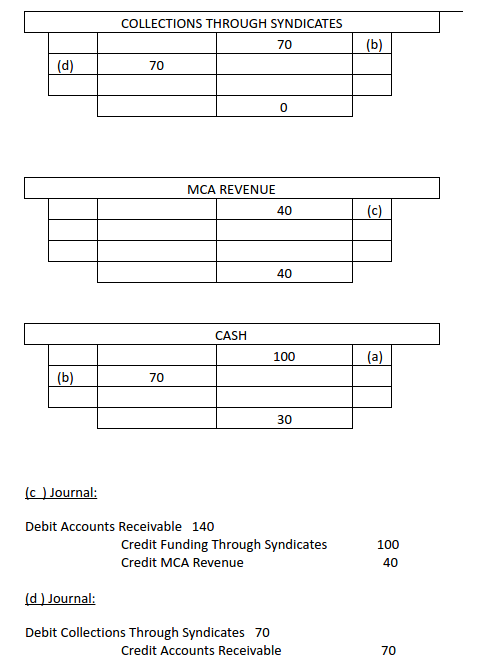

First, we start by looking at an entity who sends funds to an MCA company. As this is where the money trail starts, this is where we will start as well. When a syndicator sends funds to an MCA company they should set up a temporary ledger account. We usually call this “funded thru syndicates”. Every time they send money to the MCA company this entry will show a credit to cash and a debit to this temp account. It won’t have any meaning now but it will have a lot of meaning at the end of the year when they need to produce their financial statements. When this syndicator receives back their money they should debit cash and credit a different account. We usually call this different account ‘collections through syndicates’.

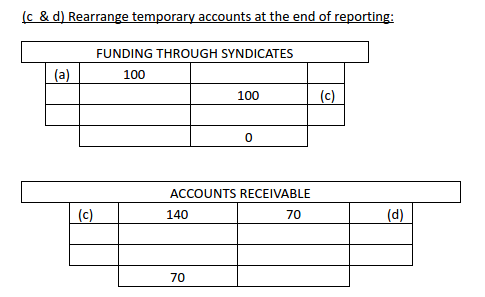

Now, the number of this type of transaction is going to depend entirely on how many deals the syndicator gets involved with and how often they receive cash back from the MCA company. Let’s say there are an accumulation of small transactions that happen over the year. Their outcome is going to be that their ‘funding through syndicate’ account is going to have a debit balance. For the sake of this example, we will make that debit balance 100k. Their ‘collections thru syndicate’ account is going to have a collective credit balance. For this example we will say the credit balance is 70k. As we said, these transactions will not have much meaning when you are processing them individually, but now they will show the bigger picture to your accountant (and hopefully to you!).

The ‘funded through syndicate’ account is at 100k because the syndicator provided the MCA company with 100k (which then went to merchants). Of course, they are not only getting 100k back. In this business the syndicators must make money on the funds they provide. For the sake of this example, the syndicator will look to get back 140k. Now you see that balance outstanding is 70k.

The MCA receivable has a debit balance of 70k, which is what they owe and their revenue is 40k. That’s the difference between the 140k and the 100k.

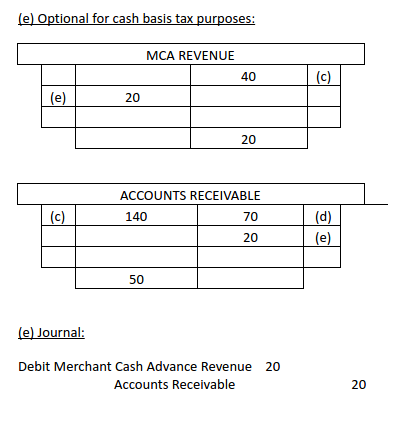

Now the temp accounts are down to zero. The next step looks at the 70k receivable. We know that 20k of it is uncollected revenue. Based on what we have before, which is used for cash basis purposes, I will add another journal entry crediting merchant cash receivable 20k. This will bring down my receivable to 50k which represents the principal portion of the 100k. This shows the syndicator gave the MCA company 100k and half of it is collected. Now we debit MCA revenue and that brings down the syndicator’s revenue from 40k to 20k for cash basis.

As far as GAAP is concerned we don’t have special guidance for this industry. The industry is very unique. We do have the principal of industry practices constraint. I have been very involved in this industry for years. I had a lot of talks with dozens of people all over the country. Investors, funders, creditors, ISO’s, professionals, etc, basically all walks of life connected to this industry. I do feel and believe that the way everyone wants and expects to see the reporting is the way I explained it. As far as MCA companies are concerned they do recognize revenue when your performance obligation has been completed; that is funding. Everything the funder does in the future is collecting their money. There is no performance that this merchant wants from the funder. As a matter of fact the merchant (customer) would be very happy if the funder ceases his activity which is strictly collections. In all other cases where we see revenue being deferred the company still has an obligation to perform. For example, prepaid phone service or insurance both provide services after the bill has been paid. Regarding uncertainty, I feel that this is no different than uncollected receivables. This is why we have a bad debt provision. The bad debt is based on historical performance of each one’s experience. As a side note, I do see a pretty consistent ratio across the line. Uncertainty leads you to the subject of derivatives. Derivatives are uncertain and unknown. Everything is underlined by a future event in the market value of a later date. This is different, as I explained. For instance, a grocery store’s AR is not certain in regards to how much they are going to collect. That is why we always work with fair estimates.

Question #7: How does this journal entry affect my tax returns? Won’t the IRS want it explained? Do they need to see it on each merchant cash advance or all in one entry?

Yoel Wagschal CPA: The IRS is not in the habit of asking to see your internal accounting unless they are performing an audit. They want to see the final result which is your tax return. This is the final report you provide to them. If you are audited then you have to substantiate your numbers and they ask for your ledger. If this happens they will see one journal entry (the one we just discussed) and they will ask how you got to those numbers. Here you will need to provide all the necessary backup, which you will undoubtedly have in your excel sheets, platforms, and correspondence. My accounting firm keeps a detailed record of all financial information we receive. When we do the final journal entry we keep and file all of the source documents that were used to calculate those numbers. We suggest you do the same not simply because the IRS may ask for them but because your investors may ask, your partners may ask, or you may need to present this information in order to diversify your business portfolio. The most important reason to have accurate and reliable financial information is, of course, that it will be used by the business owner – YOU!

Phone (845) 875-6030

Fax (845) 678-3574

Email: cjt@ywcpa.com

http://ywcpa.com

Business Loan Seekers Likely to Consider Numerous Options, Study Says

April 25, 2022 New data published in the annual FinTech Lending Study published by Smarter Loans revealed that 40% of business loan seekers compare more than six options.

New data published in the annual FinTech Lending Study published by Smarter Loans revealed that 40% of business loan seekers compare more than six options.

Though this study focused on the Canadian market, it may partially explain a finding in the US, that more small business owners seeking capital are seeking out a merchant cash advance as a potential option than ever more. (A Federal Reserve study said that 10% of SMB capital seekers sought a merchant cash advance in 2021). That would make sense if business owners are obsessively applying to multiple sources for the sake of making more comparisons.

But even while they shop, they might not always be satisfied with what they learn, nor the outcome. Smarter Loans reported that only 60% of business loan seekers felt informed about their options while 40% of business owners that went forward with a business loan were not satisfied with their loan provider.

When examining both the business loan and consumer loan market, Smarter Loans says that loan seekers are more likely to receive their funds the same day they apply than ever before. (53% of those surveyed received funds within 24 hours of applying.)

Click here To view the full 2022 FinTech Lending Study published by Smarter Loans.

2019 Top 25 Executive Leaders in Lending – Canadian Lenders Association – Presented By BMO

November 11, 2019 The Canadian Lenders Assocation (CLA) received 124 nominations for these awards from leaders in lending across the country. The CLA’s goal is to support access to credit in the Canadian marketplace and champion the companies and entrepreneurs who are leading innovations in this industry.

The Canadian Lenders Assocation (CLA) received 124 nominations for these awards from leaders in lending across the country. The CLA’s goal is to support access to credit in the Canadian marketplace and champion the companies and entrepreneurs who are leading innovations in this industry.

The Top 25 finalists in this report represent various innovations in the borrower’s journey from innovations in artificial intelligence powered credit modelling to breakthroughs in consumer identity management using blockchain technologies. These finalists also represent solutions for a wide spectrum of borrower maturity and needs, ranging from consumer credit rebuilding all the way to senior debt placements for global technology ventures.

See The Leading Companies Report Here

See The Leading Executives Report Here

|

Mark Cashin

CEO of myBrokerBee | Ontario After a career in commercial finance and being CEO of Transpor, Mark Co-founded myBrokerBee a mortgage broker platform that provides transparency to private lenders and their clients. |

|

Avinash Chidambaram

CEO of Ario Platform | Ontario Through his experience as Product lead at Interac and Blackberry, Avinash has helped bring together an accomplished and talented group of experts in Data Science, Machine Learning, Security, Software Development to successfully develop this banking services software platform Ario. |

|

Evan Chrapko

CEO of Trust Science | Alberta Evan is the founder and CEO of Trust Science, a leader in organizing alternative credit data. As a saas founder and CEO, Evan has done over 500mm in startup exits. |

|

Kevin Clark

President of Lendified | Ontario Kevin is a recognized leader in the financial services industry with over 30 years of experience. Kevin has helped create the voice of Canada’s SME lending ecosystem through his leadership of Lendified and the CLA. |

|

Jerome Dwight

VP of Cox Automotive | Ontario Jerome established Nextgear Capital in Canada to become the largest specialty finance company in the automotive sector. Jerome is a Globe & Mail 40 under 40 winner and previously lead RBC’s international wealth management, private banking and asset servicing business. |

|

Saul Fine

CEO of Innovative Assessmer | Israel Saul is a licensed organizational psychologist and psychometrician, and a former lecturer in psychology at the University of Haifa. Saul is a global leader in the use of psychometric data for credit scoring and financial inclusion. |

|

David Gens

CEO of Merchant Growth | BC David is the Founder and CEO of Merchant Growth, which grew from its humble beginnings in his apartment to offices in both Toronto and Vancouver. David now leads one of Canada’s largest online small business finance companies. |

|

Bryan Jaskolka

COO of CMI | Ontario Nominated for the 2018 Mortgage Broker of the Year, Bryan Jaskolka is an expert in Canadian mortgage financing with a particular focus on the alternative lending space and mortgage investing. |

|

Peter Kalen

CEO of Flexiti | Ontario Peter is a leader in Canada’s retail financing market. Before founding Flexiti, Peter was in senior leadership positions at Citi, PC Financial, and Sears Canada. Flexiti was recently named #7 on the Deloitte Fast50. |

|

Yves-Gabriel Leboeuf

CEO of Flinks | Quebec Yves-Gabriel Leboeuf is the co-founder and CEO of Flinks. Under his leadership, Flinks has become a Canadian leader in banking data enablement. |

|

Derek Manuge

CEO of Corl | Ontario Derek, also known as the “the quant from Canada” is the founder of the data-driven venture firm, Corl. Corl is one of Canada’s leaders in the use revenue-share financing models. |

|

Keren Moynihan

CEO of Boss Insights | Ontario Keren Moynihan is co-founder and CEO of Boss Insights, a company that uses big data and AI to accelerate lending from months to minutes. With a Joint JD/MBA, Keren has a diverse background as a commercial banker, wealth manager and former founder of an impact startup. |

|

Jason Mullins

CEO of Goeasy | Ontario Jason is President and CEO of goeasy, a publicly listed consumer lender. Jason has lead the company to become one of the largest and most innovative lenders in the country. |

|

Paul Pitcher

CEO of SharpShooter Funding | Ontario After founding First Down Funding, an alternative lending firm for SMEs in Baltimore, Paul expanded his business to Canada through the subsidiary Sharpshooter Funding. |

|

Brendan Playford & Cate Rung

Co-Founders of Pngme | USA Cate, ex-Uber and Brendan, a blockchain and agro-finance entrepreneur are the co-founders of Pngme, an alternative lending platform for financial institutions in emerging markets who serve Micro, Small, and Medium-sized Enterprises. |

|

Wayne Pommen

CEO of Paybright | Ontario Wayne is the President and CEO of PayBright. Wayne is also a director of IOU Financial Inc and of HBC. Previously, Wayne was a Principal at TorQuest Partners, one of Canada’s leading private equity firms, and a management consultant with Bain & Company in the UK, the US, and Canada. |

|

Adam Reeds

CEO of Ledn | Ontario Adam is a pioneer and thought leader in the digital asset backed lending space. Ledn is focused on building innovative financial products in the emerging digital asset space, with a focused mission to help people save more in bitcoin. |

|

Adam Rice

CEO of LoanConnect | Ontario Adam has played a pivotal role in building one of the largest online markets in Canada for unsecured loans. |

|

Mark Ruddock

CEO of BFS Capital | Ontario Mark is an experienced international CEO with two successful exits and over 20 years of experience at the helm of VC backed technology and fintech startups. In 2019 Mark announced BFS Capital’s expansion to Canada with a new 50 engineer data science hub in the heart of Toronto. |

|

Vlad Sherbatov

President of Smarter Loans | Ontario Vlad Co-founded Smarter Loans in 2016 with the goal of helping Canadians make smarter financial decisions. Since then, Vlad has grown the platform into one of the go-to resources for Canadian borrowers. |

|

Steven Uster

CEO of FundThrough | Ontario Steven is the Co-Founder & CEO of FundThrough, an invoice funding service that helps business owners eliminate “the wait” associated with payment terms by giving them the power and flexibility to get their invoices paid when they want, with one click, and in as little as 24 hours. |

|

Dmitry Voronenko

CEO of Turnkey Lender| Singapore Dmitry, CEO and Co-founder of TurnKey Lender, holds a PhD in Artificial Intelligence. Dmitry was recently named SFA’s Fintech Leader of the year. |

|

Neil Wechsler

CEO of Ondeck Canada | Quebec Neil briefly practiced law before becoming President and CEO of Optimal Group Inc. where he grew the company from a start-up to a leading NASDAQ-listed self-checkout and payments company. Neil later co-founded Evolocity, which in 2019 became OnDeck Canada. |

|

Michael Wendland

CEO of Refresh | BC Michael has led Refresh Financial’s rapid growth since its founding in 2013, including a recent ranking of number 40 on Deloitte’s Fast 500. |

Canadian Lender’s Association Awards Leading Executives and Companies

November 11, 2019 Today the CLA announced the winners for its 2019 Leaders in Lending Awards. Highlighting the efforts of exceptional players within the fintech and alternative finance fields, the awards seek to “celebrate the industry and celebrate all the cool fintech things happening in Canada,” according to the CLA’s Strategic Partnerships Director Tal Schwartz.

Today the CLA announced the winners for its 2019 Leaders in Lending Awards. Highlighting the efforts of exceptional players within the fintech and alternative finance fields, the awards seek to “celebrate the industry and celebrate all the cool fintech things happening in Canada,” according to the CLA’s Strategic Partnerships Director Tal Schwartz.

Now in its second year, the Leaders in Lending Awards are split into two categories, with one focusing on the efforts of companies in the industry and the other on individual executives. 2019 will be the first year that the latter of these categories is incorporated. The awards will be imparted to their new owners at the Canadian Lenders Summit later this month, where a special prize will also be given to one winner from each category.

Among the winners in the first category are Borrowell, IOU Financial, and Michele Romanow’s Clearbanc. While making an appearance in the second category are David Gens of Merchant Growth, Paul Pitcher from SharpShooter Funding, Smarter Loans’ Vlad Sherbatov, and Kevin Clark from Lendified.

The criteria for the awards were based upon three tenets, these being a commitment to the “use of advanced fintech solutions” to solve challenges in the lending process, the “implementation of new or innovating lending strategies or business models,” and evidence of successful outcomes following the implementation of new fintech or a new business model.

When asked about possible expansions to the awards in the future, Schwartz was receptive to the idea of covering more ground with the prizes, saying “I definitely think we’ll expand the categories.” Mentioning that there’s a host of niches that are worth highlighting, such as blockchain, psychographic credit scoring, and credit rebuilding, which deserve their day in the sun.

“We have a mandate as a trade group to celebrate the industry,” emphasized Schwartz. And that celebration will be taking place on November 20th at the Canadian Lenders Summit in Toronto.

Consultative Selling in Small Business Finance

October 16, 2019

It’s nearly impossible to teach fiscal responsibility to most consumers, according to researchers at universities and nonprofit agencies. But alternative small-business funders and brokers often manage to steer clients toward financial prudence, and imparting pecuniary knowledge can become part of a consultative approach to selling.

It’s nearly impossible to teach fiscal responsibility to most consumers, according to researchers at universities and nonprofit agencies. But alternative small-business funders and brokers often manage to steer clients toward financial prudence, and imparting pecuniary knowledge can become part of a consultative approach to selling.

Still, nobody says it’s easy to convince the public or merchants to handle cash, credit and debt wisely and responsibly. Consider the consumer research cited by Mariel Beasley, principal at the Center for Advanced Hindsight at Duke University and co-director of the Common Cents Lab, which works to improve the financial behavior of low- and moderate-income households.

“For the last 30 years in the U.S. there has been a huge emphasis on increasing financial education, financial literacy,” Beasley says. But it hasn’t really worked. “Content-based financial education classes only accounted for .1 percent variation in financial behavior,” she continues. “We like to joke that it’s not zero but it’s very, very close.” And that’s the average. Online and classroom financial education influences lower-income people even less.

The problem stems from trying to teach financial responsibility too late in life, says Noah Grayson, president and founder of Norwalk, Conn.-based South End Capital. He advocates introducing young people to finance at the same time they’re learning history, algebra and other standard subjects in school.

Yet Grayson and others contend that it’s never too late for motivated entrepreneurs to pick up the basics. Even novice small-business owners tend to possess a little more financial acumen than the average person, they say. That makes entrepreneurs easier to teach than the general public but still in need of coaching in the basics of handling money.

Take the example of a shopkeeper who grabs an offer of $50,000 with no idea how he’ll use the funds to grow the business or how he’ll pay the money back, suggests Cheryl Tibbs, general manager of One Stop Commercial Capital, Douglasville, Ga. “The easy access to credit blinds a lot of merchants,” she notes.

Entrepreneurs often make bad decisions simply because they don’t have a background in business, according to Jared Weitz, CEO of New York based United Capital Source. “Many of the people who come to us are trying their hardest,” he observes.

Entrepreneurs often make bad decisions simply because they don’t have a background in business, according to Jared Weitz, CEO of New York based United Capital Source. “Many of the people who come to us are trying their hardest,” he observes.

Weitz offers the example of his own close relative who’s a veterinarian. That profession attracts some of the brainiest high-school valedictorians but doesn’t mean they know business. “He’s the best doctor ever and he’s not a great businessman because he doesn’t think about those things first. What he thinks about is helping people. That’s why he got into his profession.”

Entrepreneurs often devote themselves to a vision that isn’t businesses-oriented. “They start a business because they have a great idea or a great product, and that’s what excites them,” Grayson says. “They jump in with both feet and don’t think much about the business side.” The business side isn’t as much fun.

Merchants also attend to so many aspects of an enterprise—everything from sales, production and distribution to hiring, payroll and training—that they can’t afford to devote too much time to any single facet, notes Joe Fiorella, principal at Kansas City, Mo.-based Central Funding. Business owners respond to what’s most urgent, not necessarily what’s most important.

For whatever reason, some business owners spiral downward into financial ruin, bouncing checks, stacking merchant cash advances and continually seeking yet another merchant cash advance to bail them out of a precarious situation, says Jeremy Brown, chairman of Bethesda, Md.-based Rapid Advance.

Weitz advises sitting down with those clients and coming to an understanding of the situation. In some cases, enough cash might be coming in but the incoming autopayments aren’t timed to cover the outgoing autopayments, he says by way of example.

Informing clients of such problems makes a demonstrable difference. “We can see that it works because we have clients renewing with us,” says Weitz. “We’re able to swim them upstream to different products” as their finances gradually improve, he says.

The products in that stream begin with relatively higher-cost vehicles like merchant cash advances and proceed to other less-expensive instruments with better terms, says Brown. Those include term loans, Small Business Administration loans, equipment leasing, receivables factoring and, ultimately the goal for any well-capitalized small business—a relationship with the local bank.

Failing to consider those options and instead simply abetting stackers to make a quick buck can give the industry a “black eye,” and it benefits none of the parties involved, Tibbs observes. But merchants deserve as much blame as funders and brokers, she maintains.

Prospective clients who stack MCAs, don’t care about their credit rating and simply want to staunch their financial bleeding probably account for 35 percent to 40 percent of the applicants Tibbs encounters, she says.

Just the same, alt-funders continue to urge clients to hire accountants, consult attorneys, employ helpful software, shore up credit ratings, keep tabs on cash flow, calculate margins, improve distribution chains and outline plans for growth. It’s what helps the industry rise above the “get-money quick” image that it’s outgrowing, Weitz, says. Many funders and brokers consider providing financial advice an essential aspect of consultative selling. It’s an approach that begins with making sure applicants understand the debt they’re taking on, the terms of the payback and how their businesses will benefit from the influx of capital. It continues with a commitment to helping clients not just with funding but also with other types of business consultation.

“It’s not so much selling as building a rapport with clients—serving as a strategic advisor or financial resource for them, identifying their needs and directing them to the right loan product to meet those needs,” says Grayson. “They should feel they can call you about anything specific to their business, not just their loan requests.” He also cautions against providing information the client will not absorb or will find offensive.

Justin Bakes, CEO of Boston-based Forward Financing also advocates consultative selling. “It’s all about questions and getting information on what’s driving the business owner,” he says. “It’s a process.”

Consultative sales hinges on knowing the customer, agrees Jason Solomon, Forward Financing vice president of sales. “Businesses are never similar in the mind of the business owner,” he notes. “To effectively structure a program best-suited to the merchant’s long-time business needs and set a proper path forward to better and better financial products, you need to know who the business owner is and what his long term goals are.”

“It’s taking an approach of actually being a consultant as opposed to a $7 an hour order taker,” Tibbs says of consultative selling. “I like to teach new reps to think of it as if you were a doctor. Doctors ask questions to arrive at a final diagnosis. So if you’re asking your prospective customer questions about their business, about their cash flow, about their intentions of how they’re planning to get back on track.”

Learning about the clients’ business helps brokers recommend the least-expensive funding instrument, Tibbs says. “I really hate to see someone with a 700 credit score come in to get a merchant cash advance,” she maintains. The consultative approach requires knowing the funding products, knowing how to listen to the customer and combining those two elements to make an informed decision on which product to recommend, she notes.

Consultative sales can greatly benefit clients, Weitz maintains. If a pizzeria proprietor asks for an expensive $50,000 cash advance to buy a new oven, a responsible broker may find the applicant qualifies for an equipment loan with single-digit interest and monthly payments over a five-year period that puts less pressure on daily cash flow.

Consultative sales can greatly benefit clients, Weitz maintains. If a pizzeria proprietor asks for an expensive $50,000 cash advance to buy a new oven, a responsible broker may find the applicant qualifies for an equipment loan with single-digit interest and monthly payments over a five-year period that puts less pressure on daily cash flow.

It’s also about pointing out errors. Brokers and funders see common mistakes when they look at tax returns and financial records, says Brown. “The biggest issue is that small-business owners—because they work so hard— make a profit of X amount of money and then take that out of the business,” he notes. Instead, he advises reinvesting a portion of those funds so that they can build equity in the business and avoid the need to seek outside capital at high rates.

Another common error occurs when entrepreneurs take a short-term approach to their businesses instead of making longer-term plans, Brown says. That longer-term vision includes learning what it takes to improve their businesses enough to qualify for lower-cost financing.

Sometimes, small merchants also make the mistake of blending their personal finances and their business dealings. Some do it out of necessity because they’re launching an enterprise on their personal credit cards, and others act of ignorance. “They don’t necessarily know they’re doing something wrong,” Grayson observes. “There are tax ramifications.”

Some just don’t look at their businesses objectively. Take the example of a company that approached Central Funding for capital to buy inventory in Asia. Fiorella studied the numbers and then informed the merchant that it wasn’t a money problem—it was a margins problem. “You could sell three times what you’re wanting to buy, and you still won’t get to where you want to be,” he reports telling the potential customer.

Consultative selling also means establishing a long-term relationship. Forward Financing uses technology to keep in contact with clients regularly, not just when clients need capital, Bakes notes. That cultivates long-lasting relationships and shows the company cares. As the relationship matures it becomes easier to maintain because the customers want to talk to the company. “They’re running to pick up the phone.”

The conversations that don’t hinge on funding usually center on Forward Financing learning more about the customer’s business, says Solomon. That include the client’s needs and how they’ve used the capital they’ve received.

“We have our own internal cadence and guidelines for when we reach out and how often and what happens,” says Solomon. Customer relationship management technology provides triggers when it’s time for the sales team or the account-servicing team to contact clients by phone or email.

Do small-business owners take advice on their finances? Some need a steady infusion of capital at increasingly higher cost and simply won’t heed the best tips, says Solomon. “It’s certainly a mix,” he says. “Not everybody is going to listen.”

Paradoxically, the business owners most open to advice already have the best-run companies, says Fiorella. Those who are closed to counseling often need it the most, he declares.

Moreover, not everybody is taking the consultative approach. “New brokers are so excited to get a commission check they throw the consultative approach out the window,” Tibbs says.

Yet many alt-funders bring consultative experience from other professions into their work with providing funds to small business. Tibbs, for example, previously helped home buyers find the best mortgage.

Consultative selling came naturally to Central Funding because the company started as a business and analytics consultancy called Blue Sea Services and then transformed itself into an alternative funding firm, says Fiorella. Central Funding reviews clients’ financial statements and operations between rounds of funding, he notes.

Consultations with borrowers reach an especially deep level at PledgeCap, a Long Island-based asset-based lender, because clients who default have to forfeit the valuables they put up as collateral—anything from a yacht to a bulldozer—says Gene Ayzenberg, PledgeCap’s chief operating officer. Conversations cover the value of the assets and the risk of losing them as well as the reasons for seeking capital, he notes.

No matter how salespeople arrive at their belief in the consultative approach, they last much longer in the business than their competitors who are merely seeking a quick payoff, Tibbs says. Others contend that it’s clearly the best way to operate these days.

“The consultative approach is the only one that works,” says Weitz. “Today, everything is about the customer experience. People are making more-educated, better informed decisions.” What’s more, with the consultative approach clients just keep getting smarter, he adds.

The days of the hard sell have ended, Grayson agrees. Customers have access to information on the internet, and brokers and funders can prosper by helping customers, he says. “Our compensation doesn’t vary much depending upon which product we put a client in so we can dig deeper into what will fit the client without thinking about what the economic benefit will be to us.”

Even though the public has become familiar with alternative financing in general, most haven’t learned the nuances. That’s where consultative selling can help by outlining the differing products now available for businesses with nearly any type of credit-worthiness. “It’s for everybody,” Weitz says of today’s alternative small business funding, “not just a bank turn-down.”

Making it Work: CanaCap and the Case for Canada

July 5, 2019 What leads an alternative financer to establish their own business in Canada? For Evan Marmott and his partner Adam Benaroch, it was the level of opportunity that the country offered in comparison to United States, where the alternative funding industry had become bloated and saturated with funders and brokers alike by 2017, when the pair established CanaCap.

What leads an alternative financer to establish their own business in Canada? For Evan Marmott and his partner Adam Benaroch, it was the level of opportunity that the country offered in comparison to United States, where the alternative funding industry had become bloated and saturated with funders and brokers alike by 2017, when the pair established CanaCap.

Holding over 30 years of experience in alternative finance between them, Marmott and Benaroch founded CanaCap with the intention of capitalizing off interested Canadian merchants that were much more receptive to the message of brokers and funders. Not being bombarded by constant emails and advertisements for quick loans, Marmott says, leads Canadian business owners to be more open-minded to discussing alternative funding with brokers, resulting in both a better understanding of the conditions of the financing as well as more time on the phone to make deals. And on top of this, the lack of a dominant player within the alternative funding world of Canada leads to a divided market share, allowing small and large firms alike to succeed.

Accompanying this advantage of time and space within the market is the quality of merchants found in Canada. Claiming that Canadian merchants generally perform better than American business owners when repaying debts, Marmott explains that funders operating north of the border can expect to have a “cleaner” portfolio.

And lastly, the level of product knowledge amongst potential customers appeared to be just right to Marmott and Benaroch. With the former noting how CanaCap is unique in its willingness to offer second positions to Canadian businesses, Marmott highlights how his company benefits from larger financers, such as OnDeck, who many of their customers would go to first, learn about the funding process, be denied funds, and then be picked up by CanaCap after further researching the industry.

With offices in both Montreal and New York, the latter of these being for CapCall, the American counterpart to CanaCap, Marmott is well-attuned to the differences between the two markets. And while he concedes that the downside of brokering in the Great White North is the 30% that is clipped from commissions due to currency exchange, he affirms that the savings from reduced marketing costs, providing better return on investment rates, offset this loss.

Altogether, the CEO makes a convincing case for why one should consider alternative financing in Canada. Taking the tack that the country provides a fresh slate of sorts to financers, where merchants have yet to be inundated with offers, promotions, and horror stories about the industry, Marmott and Benaroch have enjoyed success with their model of approving over 90% of their applicants and streamlining the application process as to increase turnaround times.

With plans to stay put for the foreseeable future, Marmott says that he’s “looking forward to funding small businesses” as his company continues to service the entire country and the alternative finance industry in Canada develops. A plan that doesn’t sound too bad, especially with signs pointing towards increased growth and further interest from merchants.

2M7 Financial Solutions and the State of Alternative Funding in Canada

July 1, 2019 “What’s a cash advance?”

“What’s a cash advance?”

This is how Avi Bernstein, CEO of 2M7 Financial Solutions, recalled a typical conversation in 2008, when his company was founded in the Canadian market. According to him, customer knowledge of alternative financing methods was dismal, partly due to a handful of homogenous banks dominating the scene as well as a void of funders in the country.

Flash forward to 2019 and 2M7 is operating within a Canadian market that is much more trusting and knowledgeable of merchant cash advances, although it is not yet at the levels witnessed in the U.S.

“Low hanging fruit,” is how Bernstein describes the industry now, as small and medium-sized businesses are flocking to 2M7 and its contemporaries, which offer higher approval ratings and faster confirmation of funding than their more traditional counterparts. In fact, according to a 2018 study conducted by Smarter Loans, 24% of those Canadians surveyed stated that they sought their first loan with an alternative lender that year. As well as this, only 29% reported that they pursued funding from more established, traditional financial institutions and 85% of those that received financing confirmed their satisfaction.

Figures like these help to explain why the Canadian market has seen a rise in interest from foreign businesses in the previous five years. Greenbox Capital, First Down Funding, and Funding Circle are examples of those companies who have successfully implanted themselves within the market, a feat that Bernstein claims isn’t easy.

“It’s a different business,” he notes when comparing the market to that of the U.S. Listing the dissimilarities in market maturity levels, sales tactics, processing channels, and collection styles, as well as the currency exchange rate that’s to be considered, Bernstein says that he’s found those American funders who come to Canada unprepared never stay long enough to become a fixture of the industry.

“It’s a different business,” he notes when comparing the market to that of the U.S. Listing the dissimilarities in market maturity levels, sales tactics, processing channels, and collection styles, as well as the currency exchange rate that’s to be considered, Bernstein says that he’s found those American funders who come to Canada unprepared never stay long enough to become a fixture of the industry.

Warning against half measures, Bernstein explains that “You’ve gotta put boots on the ground” if you want to succeed in Canada. Giving the impression that unless you’re willing to learn the rules applied in the market, hire people, and house them in an office north of the American border, Bernstein is keen to highlight what’s required of foreign companies looking with interest at Canada.

But it’s a risk-reward situation. The market is opening up as more funders enter it, and with the arrival of larger companies, such as OnDeck Capital, more resources are being devoted to raising awareness of alternative financing amongst Canadians.

Meanwhile, homogenous firms like 2M7 are continuing to grow in this developing market. Receiving an average of 200-300 applications for funds per month, 2M7 is capitalizing off opportunities by proving themselves to be open to a wider range of applications. Bernstein asserts that “we try to fund everything,” and that they keep an “open mind to every opportunity” that lands on their desk. Perhaps this is a mindset not shared by more conservative of funders in the industry, but, as Bernstein says, “we’re here, we’re funding, and we’re ready to rock n’ roll.”

You can meet Avi Bernstein and 2M7 at deBanked CONNECT Toronto on July 25th.

FUNDED $40K Towing Company in Michigan... the smarter merchant is ready to fund if you have any submissions, please call me to discuss (212.803.3320 x110 ) or email joseph@thesmartermerchant.... |

FUNDED $75K Restaurant in Texas... the smarter merchant is ready to fund if you have any submissions, please call me to discuss (212.803.3320 x110 ) or email joseph@thesmartermerchant.... |

Trying To Finish Up the Month Strong... funded $30k liquor store in louisiana thank you all the submissions and getting these deals funded. the smarter merchant is ready to fund if you hav... |

See Post... the smarter merchant - mixed sentiment whether or not they are currently funding, , other funders that mentioned they will entertain weekly:, 24 capital, clearfund solutions, east shore equities, irm capital, lending valley, queen funding, tvt capital, unique funding solutions, vitalcap fund, , confirmed seen queen doing a bunch of weeklies recently.... |

See Post... the smarter merchant - mixed sentiment whether or not they are currently funding, , other funders that mentioned they will entertain weekly:, 24 capital, clearfund solutions, east shore equities, irm capital, lending valley, queen funding, tvt capital, unique funding solutions, vitalcap fund... |

See Post... the smarter merchant - mixed sentiment whether or not they are currently funding... |